Updates: TerraVest, Seaport Entertainment, XPEL (TVK.TO, SEG, XPEL)

Latest insights on TVK, SEG, XPEL

Recent articles: XPEL’s Dealer Conference, Judges Scientific Recovery?, 2026 outlooks for TerraVest and Watches of Switzerland.

See the Table of Contents for a list of all published articles, grouped by stock.

Hidden Gems Investing has reached over 7,000 free subscribers and 300 paid members in the 15 months since the newsletter was launched. Thank you. Most of our reports require well over 100 hours of work and thousands of dollars in research expenses. A subscription gives you all of that for just $397/year, saving you enormous time and cost and protecting you from future price rises. Join our members by upgrading below, or go here to learn about what you can expect as a paid subscriber:

Seaport Entertainment (SEG)

More background: Special Report, Podcast

Seaport made two important announcements in the last couple of weeks:

The sale of 250 Water St was completed for $142mm

The Tin Building has been shut and leased to Balloon Museum

I will cover these announcements in more detail in an update after Q4 results which are being announced this week, but overall I think these two events remove most of the risk associated with investing in the company and give it a clear path to profitability.

Net of Q4 cash burn and taxes on the 250 sale, I estimate Seaport now has $175mm of cash and $50mm of debt and preferred equity. Its market cap today is $295mm and before these announcements it was $250mm. The remaining properties net of capitalized corporate expenses are worth over $500mm in my view.

The company has made big progress on cash burn since the spin-off, but the Tin Building was the one property holding it back - the building generated $-22mm in EBITDA in the last twelve months.

I think leasing the building out is the best case scenario.

Not only will the cash burn disappear overnight, Seaport will actually generate an undisclosed amount of rent from Balloon Museum when it opens this summer. Combined with a roughly $10mm swing from not having to pay interest expenses on the 250 Water St mortgage and now earning interest income on the cash that means most of the company’s cash burn has been eliminated.

Balloon Museum will also benefit the area more broadly. I argued in the Special Report that the most important thing to successfully turn around the area is creating attractions that New Yorkers are willing to walk 10 minutes from the subway for. Meow Wolf is likely to bring over 1mm visitors to the area when it opens in late 2027, while Balloon Museum attracted 300,000 visitors to a New York pop-up exhibition over 77 days in 2023.

A criticism of the Seaport area in my conversations with industry sources has been that there are too many food & beverage options in comparison to the number of visitors. Now, that is likely reversed with more visitors and the biggest source of food & beverage, the Tin Building, shut down.

The restaurants and bars at Pier 17 and the Cobblestones are likely to do very well as a result, and I would expect the company to have the area mostly leased up in the next six months or so.

That gives Seaport a clear path to profitability when Meow Wolf opens late next year.

TerraVest (TVK.TO)

More background: Special Report, 2026 outlook, Update & trade show

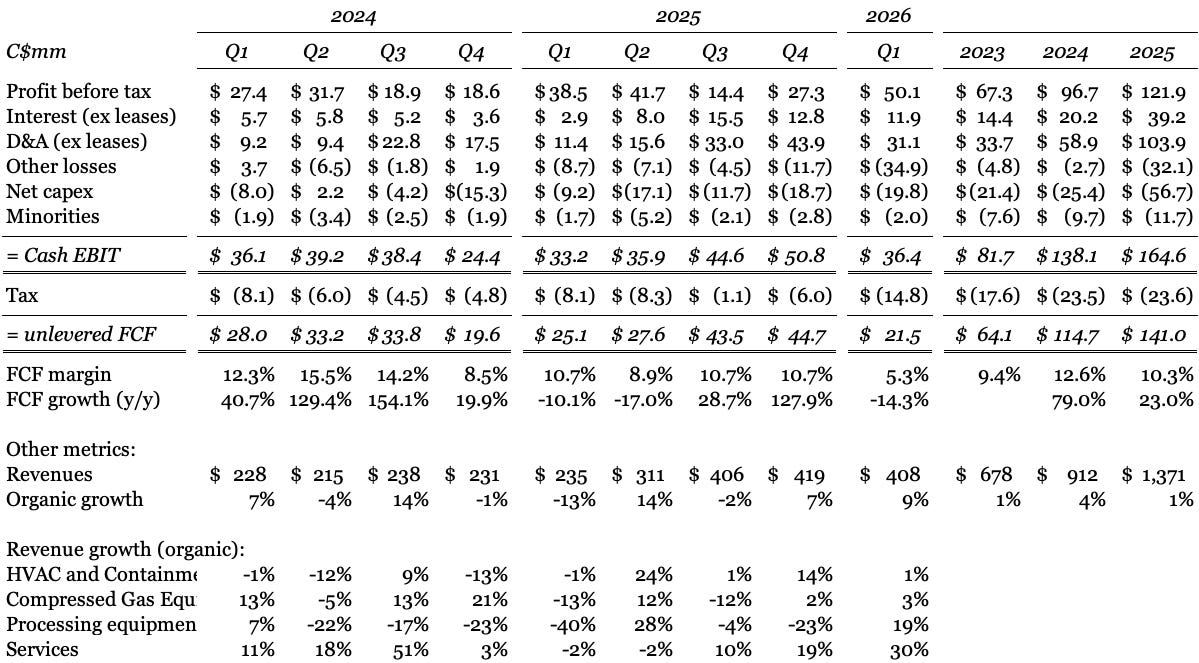

TerraVest reported a weak set of fiscal Q1 results on February 10. Organic revenue growth was +9% against a weak comp of -13%, but cash EBIT margins weakened from 14.1% to 8.9%, driven by a decline in the Entrans business that was acquired in Q2 last year:

Many of the same trends from recent quarters continued to play out:

HVAC: +1% organic growth. I am surprised that growth wasn’t much stronger against an easy comp of -1% last year considering the long order book at Highland Tank and Simplex from data centers for cooling tanks.

Compressed Gas: +3% against an easy comp of -13%. These organic numbers exclude the acquisitions of Entrans, Tankcon, and LBT. Management highlighted lower demand on tank trailers in the US, which is impacting Entrans in particular. EnTrans sales were C$115mm in the quarter, down 26% vs the C$154mm in fiscal Q1 last year, which was disclosed to SEDAR at the time of TerraVest’s acquisition.

The segment is also being impacted by an industrial slowdown in Western Canada, partly driven by tariffs and lower oil prices and highlighted by several companies. For example, Mattr (ticker: MATR), a US and Canadian manufacturer of wire and cables, highlighted “significant declines” in Canadian industrial demand late last year, which it expects will persist for several quarters.

Processing Equipment: +19% against an easy comp of -40%.

Service: +30%. This includes the Aureus and Waves acquisitions, which cannot be broken out as it is now fully integrated and boosted growth. The companies were acquired for C$28.5mm and my estimate is that true organic growth was still impressive at around +20%. The strength of the Services business over the last two years continues to significantly exceed my expectations and has boosted profitability given the segment is high margin.

The outlook statement changed significantly for the first time since FQ1 2025 (changes in bold below), suggesting a weakening of the Entrans business and strengthening of cooling tanks for data centers:

In general, TerraVest’s portfolio of businesses is performing well. Recent acquisitions have made a meaningful contribution, and we expect this to continue throughout this fiscal year. Opportunities to enhance performance through synergies between recent acquisitions and the base portfolio of businesses continue to exist and are a focus for management. Recent tariff announcements have created an environment of uncertainty in North America’s manufacturing sector. TerraVest does benefit from a diverse manufacturing footprint in North America that allows it to mitigate against direct tariff related impacts. However, this uncertainty has resulted in softer demand for certain of TerraVest’s businesses, particularly those that manufacture tank trailers. On a positive note, several of TerraVest’s portfolio companies are seeing strong demand for products related to the data center build-out in North America. The Company continues to make targeted investments to improve its manufacturing efficiency and expand its product lines, particularly in end-markets where it has a meaningful presence. With the new credit facility obtained in March 2025, TerraVest is very well-positioned to pursue its acquisition strategy.

While the quarter was fairly weak, there was a clue that one of TerraVest’s segments is about to accelerate rapidly: