Watches of Switzerland (WOSG), TerraVest (TVK) & ContextLogic (LOGC): Earnings Updates

WOSG still 13x FCF after an 85% run; TVK fuelled by data centers; LOGC's Chairman buys $5.2mm.

Recent articles:

See the Table of Contents for a list of all published articles, grouped by stock.

Hidden Gems Investing has reached over 6,700 free subscribers and 300 paid members in the 18 months since the newsletter was launched. Thank you. Most of our reports require well over 100 hours of work and thousands of dollars in research expenses. A subscription saves you enormous time and cost and protects you from future price rises. Join our members by upgrading below, or go here to learn about what you can expect as a paid subscriber:

Watches of Switzerland (WOSG.L)

More background: Special Report, 2026 outlook, Podcast

WOSG reported excellent results on May 14. Although the stock is up ~85% since I published the Special Report, I continue to believe that there is substantial upside on a three-year horizon.

Many of the risks the company has faced in the last few years (luxury slowdown, declining secondary prices, and tariffs) have reversed or are reversing. The company has demonstrated its significant resilience in the last 18 months, given these conditions, and I believe the thesis that the business has economics more similar to a subsidiary of Rolex than a retailer continues to play out. The outlook for WOSG looks stronger than it has done at any point since the report. Despite that, the stock still only trades on 13x FCF. See my 2026 Outlook for a detailed breakdown on the company’s structural growth opportunity, cycle, and valuation.

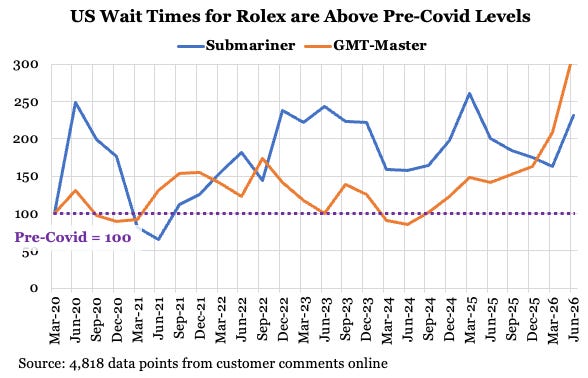

My data suggests that waiting lists continue to be very strong in the U.S:

The thesis continued to play out at fiscal H2 results:

Revenues = £983mm, +17% at constant currency (‘cc’).

Revenue from the Deutsch & Deutsch acquisition was £16mm, so organic revenue was £967mm and +15% cc. There was also an extra week which added 4%, so I estimate this was +11% cc on an underlying basis.

This was a really strong performance. They did +10% in H1 against an easy comp of +4% for a two-year stack of +14%, while H2 was +11% underlying on a tough comp of +12% for a two-year stack of +23%.

There were of course price rises in response to tariffs which boosted the revenue number maybe 5% beyond normal price rises, but that would still mean an acceleration in the two year stack to +18%. The costs of tariffs also makes the EBIT number and guidance even more impressive.

The performance was strong across the board, including the US, UK, CPO +22%, e-commerce +21% in cc.

Adj EBIT = £83.5mm-£86.5mm, -0% to +3%, 8.5%-8.8% margin vs 9.7% margin last year

Ahead of my expectations given H1 benefited from pre-tariff inventory costs but post-tariff higher prices. H2 would not have benefitted from this to such an extent.

FY adj EBIT expected to be £152-£155mm on revenues of £1,828mm for an adj EBIT margin of 8.3-8.5%. That compares to 9.1% in FY25, for a 60-80bps decline vs their guidance of 0-100bps. That guidance was made before the implementation of 31% / 39% Swiss tariffs.

US:

Revenues = £518mm, +27% at cc, +21% reported.

Adjusted for the £16mm from Deutsch & Deutsch this is £502mm or +22% cc, or +18% ex the extra week. That is incredibly impressive against a comp of +19% cc.

UK:

Revenues = £465mm, +7%.

This is an acceleration from +2% in H1 and surprising. The category is benefiting from brands releasing new watches at lower prices. The Bond St stores has also been a major success.

Outlook:

FY27 revenues +5-10% at cc. Adjusted for one less week this would have been +7-12%, and ex Deutsch (assuming £50mm FY revenue) its +5-10% again.

Adj EBIT margin expansion of 40-80bps. This was a positive surprise, as I had expected a contraction given higher COGs from tariffs. The expansion means they are getting to 8.7%-9.3%. It looks like about 20bps is from not having the Saks business go bust (which means underlying EBIT margins were even more impressive this year).

Other points:

The Roberto Coin business appears to be doing very well. WOSG has integrated Roberto Coin into Mayors, which has more than doubled their business in those stores. I expect that we will continue to see Roberto Coin rolled out across the store base.

Despite the run-up in the stock, I think it is hard to see significant downside. The company still trades on only 13x NTM FCF for mid/high single-digit organic growth and a long runway to grow in the US and deploy capital. There will also be a boost from Rolex in the next few years, which has publicly said they will increase employees by 20% its capacity expansion. That is likely to be a proxy for production growth.

I could see the stock re-rating back to 20x, which is where it used to trade.

The biggest ‘problem’ in my valuation is that with net debt down to £53mm and their amount of cash gen, they’re going to have up to £500mm acquisition capacity over the next three years (assuming they are willing to take net debt up to 1x EBITDA). It is hard to see them deploying all of that in M&A.

TerraVest (TVK.TO)

More background: Special Report, TerraVest’s next chapter, 2026 outlook

TerraVest reported a reasonable set of fiscal Q2 results. Although organic growth was -7%, this was against a tough comp of +14%. As I wrote recently in TerraVest’s Next Chapter, I believe the two big trends affecting the company are the:

Growth into new markets

Cyclical slowdown in the trailer business

Both of those trends continued in the quarter.

I believe the business is developing into four platforms:

Storage Tanks (~C$120mm EBITDA)

Led by Highland Tanks, KBK, Simplex, Mississippi Tank, Pro-par.

Traditionally driven by storage of propane and chemicals. Increasingly focused on new markets like data centers, LNG, and convenience stores.

Trailers (~C$75mm EBITDA)

Led by Entrans, Advance, LBT, Tankcon.

Transport of petroleums and chemicals. Driven by industrial cycles.

Water / Services (~C$60mm EBITDA)

Led by GES, LV, Aureus, Wave.

Water for oil & gas.

Legacy businesses (~C$50mm EBITDA)

Led by ECR, Granby, NWP.

Not a platform but a legacy group of businesses across heating oils, boilers, wellhead equipment, and others.

TerraVest does not segment its business according to these four platforms, but I still believe that the reported segments give us a clue to how each of the platforms is performing.