Inflection Points for XPEL and Douglas Dynamics (XPEL, PLOW)

PLOW raised guidance after just Q1 earnings; XPEL's OEM growth is accelerating

Recent articles: TerraVest’s Next Chapter, GCI’s Acquisition of Quintillion

Subscribe to receive updates on Seaport Entertainment and GCI Liberty this month.

See the Table of Contents for a list of all published articles, grouped by stock.

Hidden Gems Investing has reached over 6,500 free subscribers and 300 paid members in the 17 months since the newsletter was launched. Thank you. Most of our reports require well over 100 hours of work and thousands of dollars in research expenses. A subscription saves you enormous time and cost and protects you from future price rises. Join our members by upgrading below, or go here to learn about what you can expect as a paid subscriber:

Douglas Dynamics (PLOW)

More background: Special Report

PLOW reported excellent results on May 4, with the Attachments segment revenues increasing 67% y/y and the company raising full year guidance despite it only being Q1.

The stock jumped 17% on the results, but bizarrely gave it all back the next day on no new information. The silver lining is that you can now buy in for the same price having seen Q1 earnings validate the investment thesis. Read the recent Special Report for more background.

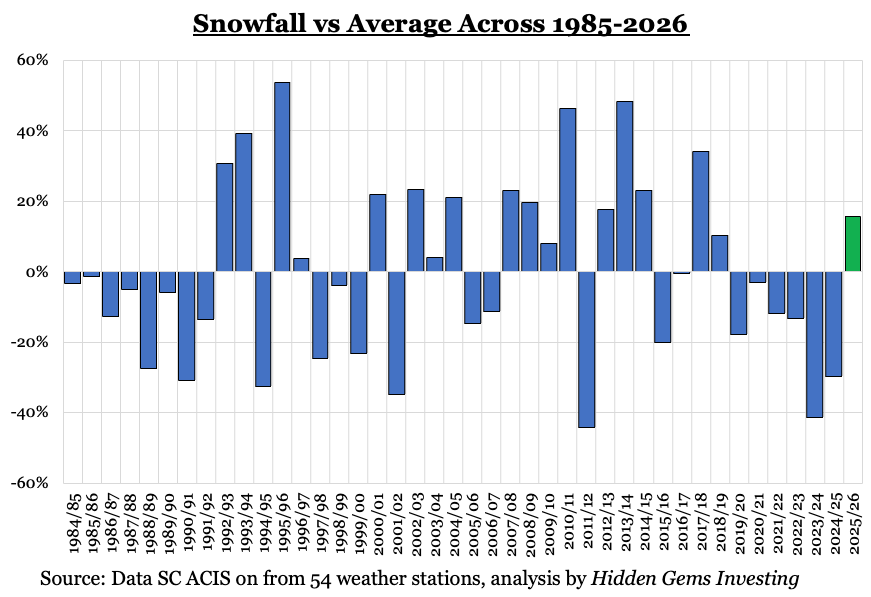

To summarize, PLOW is a good business that has been under-earning. The company is the dominant manufacturer of professional snowplows and de-icing equipment in the U.S. and Canada, with over 50% market share, but suffered from well below average snowfall between 2020-25 which masked its underlying earnings power and caused the stock to sell down.

My data and industry interviews show the 2025/26 winter season has been the strongest in almost a decade and is already acting as a catalyst to bring earnings back to normal. Earnings may even overshoot to the upside given the pent-up demand that I believe has built up. I estimate the company’s 2026 EBIT will be +54% y/y and 32% above consensus estimates.

I think Q1 results showed that it is a near certainty that this thesis is playing out to at least to some degree.

Group revenues increased 20% in the quarter, while the key snowplow Attachments business saw revenues increase 67% in its seasonally weakest quarter and EBITDA increase from $0.3mm last year to $7.7mm. In the Special Report I had estimated that Attachments revenues would increase 43% in 2026, so the +67% in Q1 and +55% in Q4 are trending well ahead of my expectations.

Management stated that:

“Our core markets experienced the heaviest snowfall in a decade this past winter, with snowfall totals approximately 25% above the 10-year average. The snowfall-driven strength of parts and accessories sales carried into the first quarter, and we are now focused on ensuring that the pre-season orders we’re currently taking for all our products are efficiently delivered to dealers in the second and third quarters of this year.”

It is important to remember the seasonality in the business. Snow falls in Q4 and Q1, and snowplow contractors tend to order parts and accessories in these quarters rather than new plows. Contractors tend to wait until winter is over before ordering plows in Q2 and Q3 to prepare for the next season.

We are therefore still early into pre-season orders, and crucially management said on the call that dealer inventories are now “solidly below” historic levels. That matches my conversations with industry sources. As one dealer told me:

“We sold 139 plows this season, the most ever in this area, I don’t think it’ll ever happen again.”

That and the pent-up demand I estimate is in the industry means I think the Bull case is now playing out. After five years of under-earning, PLOW is now benefitting from both end-user replacement demand and dealer restocking.

Consider the fact that PLOW raised group full-year adj EPS guidance by 10%, despite it being so early into the year. This is a historically conservative management team that has only recently seen pre-season orders - why would they raise guidance by 10% already? That translates to 18% group revenue growth for the year and probably 34% growth for the Attachments business. Growth over the last two quarters is well above that, and my guess is management is seeing pre-season orders which indicate that will continue through the summer.

The last time PLOW raised guidance after Q1 was in 2014, and the year ended with Attachments revenue growing 56%. That remains the biggest increase since PLOW began publishing financials in 2006. I believe 2026 is turning into a similar setup, and expect further beats and raises in Q2 and Q3.

XPEL

More background: Special Report, Manufacturing Build-Out, Growth Runway With OEMs & Color PPF

XPEL reported good Q1 results on May 6:

Revenues = $117.4mm, +13.1% y/y

US +9.9% / China +44.4% / Canada -10.9% / Europe +19.0% / Other Asia +25.1%

PPF +9.3% / Window film +24.8% / Installation +23.9%

Gross profits = $51.2mm, +16.7%, 43.6% margin

Gross margins increased 140bps y/y. Management had expected margin expansion to continue through the year, but higher oil prices, which feed into TPU and ultimately performance films, mean increasing margins are no longer guaranteed. XPEL has been conservative in pricing and may raise prices to offset increased costs.

EBIT = $13.0mm, +16.9% y/y, 11.1% margin

EBIT margins increased 40bps y/y despite sales and marketing increasing as a % of sales by 140bps. I expect margins will continue improving through the year.

Q2 guidance is for revenues to be $135-137mm, or +8.3% to +9.9%.

These results exceeded my expectations, and continue XPEL’s impressive performance in a slow market. For context, XPEL’s US revenues grew 10% when the big US auto dealers, AutoNation, Penske, and Lithia, all reported Q1 new vehicle volumes down 7-10%. Luxury vehicle imports and EV sales, both of which XPEL over-indexes to, were down far more given the expiration of EV tax credits and comparison against a strong Q1 last year when demand was pulled forward in anticipation of auto tariffs.

I would not extrapolate Q2 growth slowing to 8-10% as an indicator of XPEL’s structural growth rate, given the current environment.

As I wrote after attending XPEL’s Dealer Conference earlier this year, XPEL is significantly outperforming key competitors like SunTek and Llumar:

“In the short term, installers suggested to me that the difficult conditions over the last two years have not improved yet. While PPF customers are typically higher net worth individuals, my sense is that things may have actually gotten marginally tougher.

However, several installers told me that XPEL is doing better than its competitors, which matches what management said on the last earnings call. Many imported and challenger film brands are struggling because of tariffs, while XPEL remains significantly better than others at growing the market for its installers.”

In fact, there was a clue on the earnings call that XPEL’s structural growth thesis is playing out well.