GCI Liberty (GLIBK) Acquires Quintillion: What is John Malone up to?

8.9x EV/FCF, a distressed seller, and strategic benefits

Last week, John Malone’s GCI Liberty announced it is acquiring the Quintillion fiber network for $360mm.

Malone had given the impression that GCI would buy assets outside of Alaska, so why is he buying the Alaskan fiber network Quintillion?

I view this deal as Malone’s first step in turning GCI into his “next Liberty Media”. As I outlined in the recent Special Report, most investors think of GCI as an Alaskan telecom, but the company should instead be viewed as Malone’s next advantaged acquisition vehicle.

This article will explain:

Why I estimate the deal was done for 8.9x EV/FCF but could be as low as 6.6x

The strategic benefits to combining the companies

A clue that Quintillion may become a significant growth asset

Why I see 169% upside to GCI over the next three years

GCI Liberty (GLIBK) spun out from Liberty Broadband in July 2025, has 90% market share in its key business, and trades for 10x underlying FCF. Investors ignored the spinoff, but John Malone did not. He is Chairman, owns 7.3% of GCI, and has been buying stock. He structured the spin to turn GCI into an advantaged acquirer and “the beginning of a new Liberty Media”. We see 169% upside in our Base case.

For more background, click here to read our 30 page report on GCI, based on interviews with 17 industry sources.

Quintillion Deal Economics

GCI is buying Quintillion for an EV of $310mm + $50mm in reimbursements for capex, for an overall adjusted EV of $360mm.

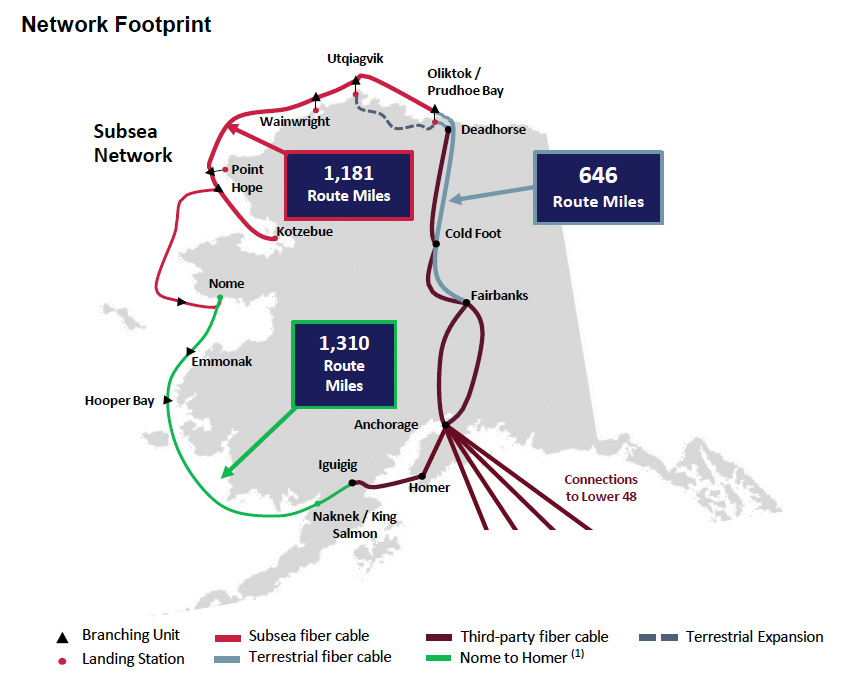

Quintillion owns a subsea fiber network in Alaska’s North Slope, going from Prudhoe Bay in the North of Alaska to Nome in the West (red line below). The company is also in the middle of extending that fiber from Nome to Homer in the South (green line).

GCI estimates that in 2026 Quintillion will generate:

Revenues of $55-60mm

Adj EBITDA of $30-35mm. Adj EBITDA was $9.2mm in Q4 2025, but that included significant add-backs for costs related to a subsea fiber cut.

Maintenance capex of $2mm

Additionally, the deal is expected to result in:

Synergies of $20mm

A $360mm step up in tax basis which can be used to offset future taxes. Assuming a 30% tax rate, that is a nominal $108mm in taxes and worth about $27mm if we take a 75% haircut to account for its present value (GCI already had a $1bn step up in basis from the spin that could be used first).

Depending on how much credit you give management on synergies and capex, this converts into a pre-tax FCF of 6.6x-11.8x. GCI has $1.36bn in tax shields post deal and accelerated depreciation from the One Big Beautiful Bill Act, so is unlikely to pay taxes for the next decade.

Here is how the valuation changes in different scenarios: