Now Unlocked: Watches of Switzerland Special Report

WOSG: A partner to Rolex trading at 12x FCF with double-digit growth

Hidden Gems Investing just crossed 6,500 free subscribers.

Thank you.

Watches of Switzerland (WOSG) stock is up ~85% since this Special Report was published, and I believe it could double again over the next three years.

I am therefore unlocking the report for all subscribers, with most of the thesis still live.

The Special Report is based on interviews with 19 industry sources and 10 store visits.

After reading this report as a primer, read my latest analysis on WOSG’s upside, results, cycle, and growth runway, based on 59 interviews over two years and attendance at the industry’s leading trade show.

Hidden Gems Investing publishes 3–4 Special Reports per year, each typically based on interviews with 20 industry sources and 100+ hours of work. Upgrade now to receive the next one in full when it drops:

This is not investment advice or a recommendation, and Plural Investing, LLC has a position in Watches of Switzerland at the time of writing. Read important disclosures here.

valuation and financials")

Situation Overview

Watches of Switzerland group (WOSG) is a retailer and partner to Rolex and other luxury watch brands. It trades on 10x FCF despite double digit growth and we think can return 35% p.a. over three years for a 145% total return.

Most of the company’s value lies in its relationship with Rolex, which only sells through authorized retailers like WOSG. That makes WOSG’s economics far superior to a typical retailer and more like a subsidiary of Rolex.

Management are competent, experienced, and well incentivized, with CEO Brian Duffy owning £30mm of stock. Duffy joined in 2014 and his strategy of investing to elevate customer experiences has grown WOSG’s share of Rolex sales in the UK from around 35% to 50%. This encouraged Rolex to entrust WOSG with replicating its strategy in the US, where it is now the number one player with 10% share and has grown at 30% p.a. for the last five years.

The stock has fallen 75% since 2022 after Rolex acquired another retailer and the luxury watch bubble burst. Investors are concerned that WOSG’s relationship with Rolex is in danger, but our work suggests it is not and that the US offers a large structural opportunity for WOSG to deploy capital at 20% returns.

Key Insights

1. WOSG is one of Rolex’s most trusted distributors, sells mostly to customers who register for a waitlist, faces no inventory risk or online competition, and has Rolex prices that only increase. WOSG’s scale gives it significant competitive advantages. (See p. 6-8, 14-17)

2. Rolex is a Swiss non-profit and we believe that the acquisition of its key Swiss retailer happened because the retailer’s founder was about to pass away and Rolex wanted to protect its distribution and maintain Swiss heritage. We do not think Rolex will disintermediate WOSG and believe that WOSG will receive increasing supply. (See p. 18-21)

3. Our data shows that Rolex waitlists have returned to normal levels and that historically Rolex has not cut production in these circumstances. In fact, Rolex plans to grow production by 60% by 2029. We think WOSG will be allocated an increasing share of that growth in the US, where purchases of luxury watches per capita are half of UK levels and most retailers are mom & pops who will struggle to compete with WOSG. (See p. 12-13, 22-25)

Research Methods

In addition to utilizing secondary sources such as company filings and transcripts, the information in this report was gathered by speaking with primary sources. This included discussions with:

Watches of Switzerland’s CEO, CFO, and IR

2 former employees at Watches of Switzerland

2 former employees at Rolex

8 former or current employees at competitors to Watches of Switzerland or Rolex

4 other relevant sources

Visits to 3 Watches of Switzerland stores and 7 competitor stores

We spoke with some sources more than once. Information that could reveal the identity of the sources above are redacted from this report unless sources gave their permission. While Hidden Gems Investing gained many insights from these conversations, no material non-public information was shared.

If you would enjoy this writeup more in a pdf format, click “Download” below:

Table of Contents

The Luxury Watch Market

Economics

Why This Opportunity Exists

Governance

Valuation

Variant View & Catalyst

The Luxury Watch Market

"Want a Rolex? Ha! A person doesn’t just buy a Rolex. There’s a process.

You’ll need to register your interest with an Official Rolex Retailer, whose window displays have a “for exhibition only” sign next to all the flashy wristwear. A salesperson will take your details while making discouraging noises about the scarcity of your preferred model, sometimes hinting that the waitlist might get shorter if you were to buy some trinkets and tchotchkes from the jewellery display.

Many months and jewellery purchases later you might hear back from the Official Rolex Retailer who’ll congratulate you on being selected to purchase a completely different model, after which you can post a “got the call!” wrist shot."

-- Financial Times, January 18, 2024

Alongside the Hermes Birkin bag or a Special Edition Ferrari, the Rolex watch is one of very few iconic products to represent the pinnacle in luxury.

From the Submariner worn by Titanic director and deep-sea explorer James Cameron to the gold Day-Dates favored by US Presidents, Rolex watches symbolize prestige.

You cannot buy a Rolex online or from Rolex itself. Instead, a select group of authorized retailers run stores in carefully chosen locations. These retailers act as gatekeepers to the Rolex universe. Supply is limited and most watches are sold to customers who have registered for a waitlist. You must build a relationship with your retailer to show that you are worthy of being selected when a Rolex becomes available. And if you quickly sell the watch on the secondary market for a substantial profit you run the risk of being banned for life.

Unlike other retailers, Rolex stores face no price competition because they strictly adhere to Rolex’s recommended retail prices. Rolex never cuts prices, they only go up over time. The waitlist means all watches are sold and there is no inventory risk. Although many customers begin their journey by learning about the watches online, stores face no online competition because that would prevent customers from being vetted and having the 'Rolex experience' in a store. That experience involves being treated to drinks or chocolates while sitting down for a consultation or on collecting a watch.

Many sources told us that being selected as a Rolex retailer is like being given a license to print money.

Watches of Switzerland is one of Rolex's most trusted retailers.

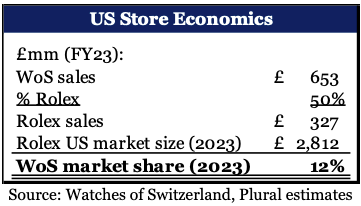

The company was Rolex’s first retail partner and their relationship goes back to 1919, not long after Rolex's founding in 1905. WoS has around half of Rolex sales in the UK. In fact, Rolex was so pleased with how WoS developed the UK market that it encouraged the company to expand into the US and grow it in a similar way. WoS is now the largest retailer in the US with around 10% share and is growing at double-digit rates.

Barriers to entry are high. Rolex increasingly only grants allocations to a few large chains like WoS who can invest millions into each store or existing mom & pop retailers who have operated for generations and have deep local customer relationships.

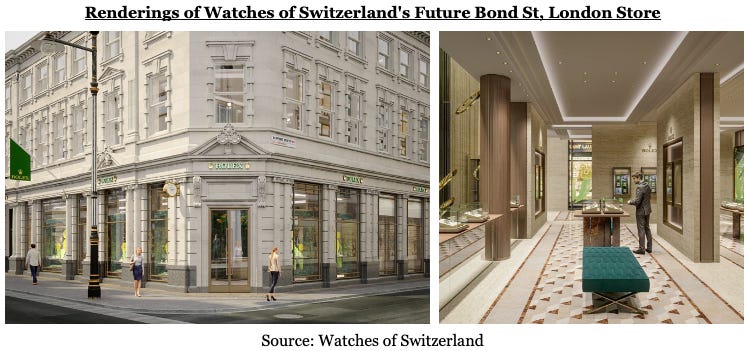

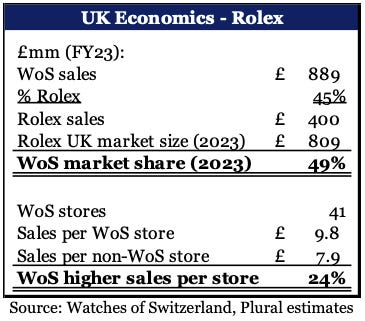

WoS's scale is a significant competitive advantage. For context, in FY23 WoS generated £890mm of revenues in the UK while the next three largest retailers generated a combined £220mm and spent £8mm in capex[1]. That £8mm of capex pales in comparison to WoS, which is increasingly spending more than that on a single store as it builds flagship locations that we would liken to a 'Disneyland of Rolex', something which virtually none of its competitors can afford. As an example, the company is replacing its existing 900 sqft Rolex boutique on Bond Street in the West End of London with a three story 8,000 sqft store dedicated entirely to Rolex. This is significant because Rolex was founded in London and the Bond Street location will become potentially the most impressive store in the world, thereby highlighting the strength of the WoS and Rolex relationship.

WoS's spending power is important because Rolex has been shrinking its retail network for decades, with the number of stores in the UK declining from 130 to 93 between 2014 to 2023. As the network continues to concentrate towards the stronger players WoS will continue to gain share.

WoS's scale and operational strength can also be highlighted in another way. Although Rolex effectively sets the prices of new watches it did introduce a Certified Pre-Owned program in late 2022 where retailers can source used watches and set their own prices when reselling them after refurbishment. In a clear sign of pricing power, WoS's large store base has enabled it to source watches and grow this program to around 7% of sales despite charging higher prices than other retailers.

Although Rolex accounts for nearly half of WoS's revenues and comes at a lower gross margin, we believe that the much higher productivity in Rolex gross profit per store and per sqft means that it actually accounts for more than half of WOS's profits and an even greater majority of its intrinsic value. This report will therefore largely focus on WoS's relationship with Rolex and why the risks investors have identified around that are misplaced.

The Luxury Watch Market

The luxury watch market is dominated by Rolex, which has around 30% share of all retail sales.

Arguably the three most prestigious major brands - Rolex, Patek Philippe, Audemars Piguet - are independent, while the others are primarily owned by Swatch, Richemont, or LVMH. Patek and AP retail prices are typically over $30,000 and they manufacture around 68,000 and 45,000 pieces per year respectively. Most of the other brands retail in the $2,000-$10,000 range and manufacture tens or hundreds of thousands of watches.

Rolex is unique in that it is the pre-eminent brand in the industry and is able to maintain its exceptional quality while making over 1mm watches. It offers watches starting around $7,000-$8000 while its most iconic pieces often retail for $30,000+.

WoS retails most of the major luxury watch brands, although Rolex sales make up nearly half of revenues. Jewelry is around another 10% of sales.

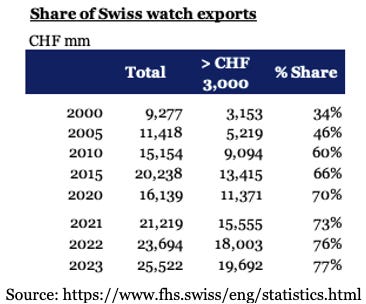

Watches over CHF 3,000 (around $3,300) make up 77% of all Swiss watch exports by value. Rolex in turn makes up around 40% of all Swiss luxury watch exports.

The importance of Rolex extends significantly further as customers often walk into a WoS store after being attracted by the Rolex brand. The Rolex halo results in customers buying other watch brands, which is why those brands like to be in a store that sells Rolex. Every industry source told us that Rolex is in a league of its own and dominates the industry. Rolex always gets the best retail space and treatment from retailers, and retailers do not know what allocation of Rolexes they will receive each year - they simply get a box and sell them.

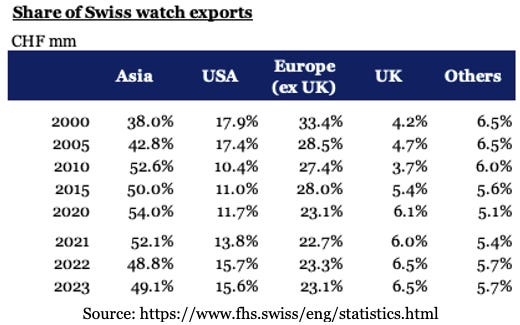

While WoS leads the UK watch retail market with half of Rolex sales by our estimates, it is important to understand the relevance of the UK market from Rolex's perspective. Rolex manufactures 1mm watches per year and allocates them across the world to its preferred market. A weak Asian market is therefore good for UK retailers for example as Rolex is likely to allocate more watches to the UK, and vice versa.

Over the last two decades Asia has increasingly become the leading market for Rolex, with Europe declining in relative terms. Despite this, the UK's share has increased by half, partly due to WoS stimulating the market through store renovations.

The US also lags behind Europe and has shown little progress, comprising half of European sales both in 2005 and today. This is something WoS is expecting to change by following the same strategy as it did in the UK.

The UK Market

The UK is one of the most mature markets in the world, with CHF 26 per capita in Swiss watch exports in 2023 vs CHF 19 in France, CHF 16 in Germany, and CHF 12 in the US.

A significant reason for the UK market's penetration has been the success of WoS's strategy. CEO Brian Duffy joined in 2014 when the company was owned by private equity firm Apollo and changed the strategy to focus on growing and stimulating the market. This has paid off, with WoS's market share increased from 32% in 2015 to 45% in 2023. Swiss watch exports to the UK grew 6.9% p.a. from 2000-15 and 5.2% p.a. from 2015-23, well above the European average of 2.3% p.a. across the 23 years.

WoS's share is likely to increase further over time as Rolex consolidates the retail base. With Rolex production increasing over at the same time the sales per showroom increased has from £1.9mm to £8.7mm between 2014 and 2023.

Continued consolidation is likely to be an even bigger tailwind for WoS in the US.

The US Market

The US market offers significant opportunity because Swiss watch exports per capita are half of the UK, at CHF 12 per capita in 2023 vs CHF 26.

Industry sources told us that while traditional brands like Rolex have a leading position in the consumer's mind, that position is less ingrained than in Europe. Newer brands, celebrities, and social media tends to have more of an influence in the US than Europe and significant marketing spend is required to impress upon consumers the unique qualities of Rolex.

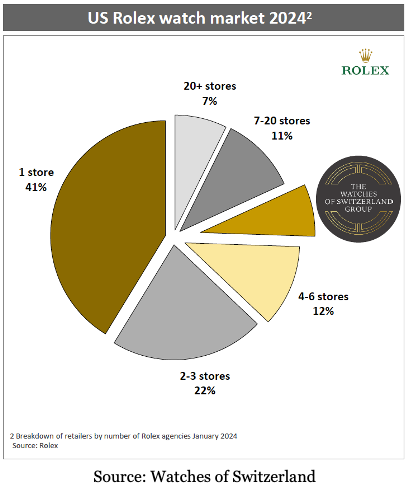

The retail market is also far more fragmented and filled with mom & pops, with WoS having the leading market share at around 10%. As Rolex increasingly demands flagship stores in the leading US cities, WoS will likely gain increasingly large allocations at the expense of mom & pops who simply cannot afford to invest the $10mm-$20mm required to build a 'Disneyland of Rolex'.

We believe WoS has faced three challenges so far in replicating its success in the US:

First, the cost of acquiring or building stores has been higher than anticipated. Many mom & pops have been reluctant to sell and held out for higher valuations, while refurbishment costs are incredibly expensive. We believe that Rolex will continue to assist WoS by pulling allocations from mom & pops if they don't sell.

Secondly, the role of luxury watches in US culture is less prominent and more marketing is required by both Rolex and WoS to stimulate demand.

Thirdly, the WoS team in the US is less experienced than the one which has had success in the UK. The CRM systems in the US are less developed, WoS is far less known, and marketing often needs to be done in a different way.

Nevertheless, our sources told us they expect WoS to be successful over time given their greater scale and the fact that no other Rolex retailer has emerged as a clear competitor.

Economics

Economic Snapshot

Unit Economics

WoS has 223 stores, with 158 in the UK, 56 in the US, and 9 in Europe that are being divested. These stores come in a whole range of sizes, but broadly fit into three categories:

~600-1,000 sqft mono-brand stores: 59 in the UK, 31 in the US, and 9 in Europe. These are typically representing less luxurious brands like TAG Heuer and generate £1mm in sales per store. They often require only 1-2 staff plus a security guard and have a lower capex requirement of £700-£1,000 per sqft.

~3,000-6,000 sqft multi-brand stores: 99 in the UK and 25 in the US. This is WoS's traditional store and about a third will have a 800-1,000 sqft Rolex shop-in-shop. Some will have shop-in-shops for other brands. These stores generate around £10-20mm in revenues, require 10-20 staff, and have a capex requirement of about £1,000 per sqft. Both the sales and capex intensity of the Rolex section are a multiple of the rest of the store, and typically most of the store's profits comes from that section.

6,000 sqft+ flagship stores: A few of the stores in the categories above we view as flagship locations that have even higher sales and capex intensity, sometimes including cocktail bars or lounge areas. An example is the 8,000 sqft Rolex-only store under construction on Bond Street that we think could cost over £15mm in capex and generate £65mm in sales. Other examples include the Audemars Piguet Town House in Manchester, UK and WoS's multi-brand stores in Soho, New York and the Wynn, Las Vegas.

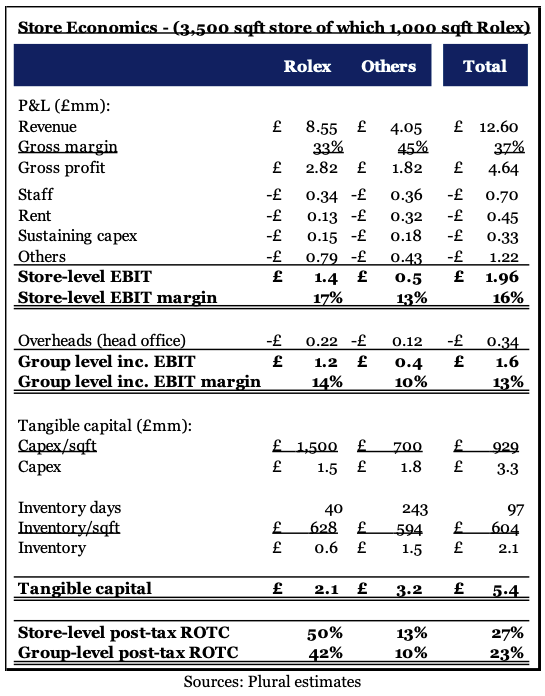

While stores vary widely, an illustrative example of a 3,500 sqft multi-brand store with a 1,000 sqft Rolex shop-in-shop shows that the economics of selling Rolex are far superior to other brands.

The sales intensity of a Rolex section is around six times higher than the other brands, illustrating the gulf in consumer desire. That results in the 1,000 sqft Rolex shop generating two-thirds of the revenues of the entire store. Even though the gross margins on Rolex are lower at 33% vs 45% for the other brands, in absolute terms that means the Rolex shop generates around 60% of the gross profit of the store or four times the gross profit per sqft.

This higher absolute level of profits is important because it results in great operating leverage and an even bigger disparity in profits at the EBIT level. The Rolex shop generates 60% of the gross profits of the store, but is only 30% of the size so only pays 30% of the rent, 30% of the utility bills, etc. We assume that it requires 5 staff vs 9 for the rest of the store and that the Rolex staff are 50% more expensive per person due to higher training and calibre requirements. We also assume that the Rolex shop has disproportionate other costs like marketing. Despite this, the much higher gross profit level drops-through to an even greater disparity in store-level EBIT. We assumed that only 50% of head office costs are variable and once allocated to the store we find that 75% of profits in the multi-brand store come from the Rolex shop.

It is worth emphasizing the insight that profit margins on a Rolex shop are higher, as the consensus among investors is that Rolex is lower margin due to the lower gross margin. We also found when speaking to industry sources that while all knew Rolex had lower gross margins, very few knew how that translated down the P&L after operating costs. Several sources accepted that the Rolex section generates more revenue than the rest of the store put together, but pushed back by pointing out it needs to because Rolex has higher requirements for staff training, marketing, and furnishing, etc, without being able to quantify the net result when weighted against the higher absolute levels of gross profit to support those expenses.

WoS said that they do not disclose EBIT margins by brand when we put our logic to them, but that margins are similar. They too pointed to higher training, marketing, and capex requirements, but said that yes they would like to have a lot more Rolex stores and that returns on capital are higher with Rolex.

We allocated £1,500 in capex per sqft to Rolex vs £700 per sqft for the other brands, but much lower inventory days given Rolexes sell off a wait list while other watches are typically in store for 6-9 months. The net result is that even though the capital requirements for Rolex are indeed higher we get a post-tax ROTC of around 40% after head office costs vs just 10% for the other brands.

Our conclusion implies that Rolex is nearly half of WoS's revenue but a larger portion of profits and returns and even larger share of intrinsic value, given we would put a higher multiple on this section of the business. We believe that that investors and the company may feel uncomfortable with Rolex being a disproportionate share of the company's value, which is partly why the company is diversifying into jewelry, which makes up over 10% of sales following the $130mm acquisition of Robert Coin in May 2024.

But we do not think a dependence on Rolex should be seen as a weakness. On the contrary, retailers are typically bad businesses. What makes WoS special is the Rolex relationship that means no online or price competition, no inventory risk, products that are effectively pre-sold and therefore profits that are largely guaranteed.

We believe that the closer WoS resembles a subsidiary of Rolex rather than a retailer the more valuable the business is.

Our conclusion can be sense-checked in several ways:

WoS discloses its non-current assets split between the UK and US, which suggests the US business has significantly higher returns on tangible capital. Rolex is a larger portion of WoS’s business in the US than the UK.

We know that Rolex revenues are around £400mm in the UK and that WoS has 41 stores selling Rolex, implying about £10mm per store. It is also an open secret in the industry that Rolex margins are about 33%, implying £3.3mm per store in gross profit. One can simply walk into WoS stores and count the number of staff, while rent per sqft within a store does not change depending on the brand. That leaves other costs as the only major swing variable and even if 100% of these and head office costs were allocated to Rolex, its return on capital would still be similar to other brands, although margins would be lower.

Retail in general has at best been a cost of capital business in recent years, so it should not be a surprise that the non-Rolex section of WoS is similar. Although luxury retail has the potential to be a better business, public peers suggest returns are still unattractive. Signet Jewellers, for instance, has generated a post-tax ROTC of 17% but this drops to 12% if assuming the company has the same inventory turns as WoS and pays higher UK tax rates.

We heard anecdotally from our sources that many brands who have tried to open their own mono-brand stores have struggled to make a profit on these stores. That has led some to turn back to working with WoS while other stores on marquee locations such as Fifth Avenue in New York have been kept open for brand building purposes. On the other hand, every single Rolex store owner we spoke with said their store was highly profitable and described getting a Rolex distribution with phrases like "a license to print money" and "the holy grail". WoS itself announced in May 2024 that it was exiting Europe, where none of its nine stores sell Rolex.

After reading this report, read my latest analysis on WOSG’s upside, results, cycle, and growth runway, based on 59 interviews over two years and attendance at the industry’s leading trade show.

Why This Opportunity Exists

Investors Greatly Overestimate the Risk of Rolex Dis-intermediating WoS

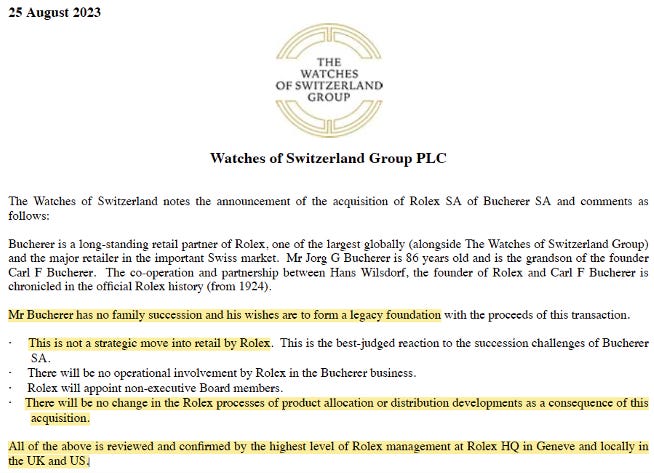

On August 24, 2023 Rolex announced that it was acquiring the retailer Bucherer. Bucherer and WoS are arguably the two most prestigious Rolex retailers, having partnered with Rolex since 1924 and 1919 respectively. Bucherer is headquartered in Switzerland and owns nearly half of the stores in Rolex's home country. It owns just 5% of distributors in the UK and US and is concentrated entirely in London in the UK.

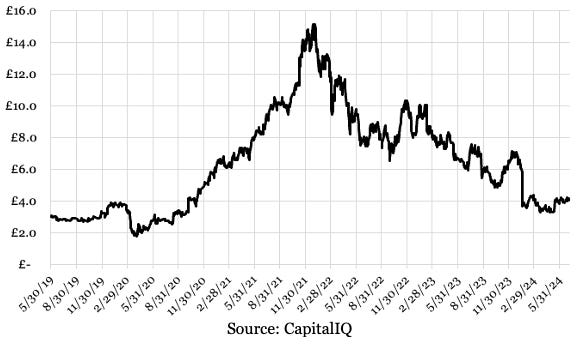

This news sent WoS shares down as much as 30% from £6.9 as investors worried that Rolex would bring retail inhouse and increasingly cut out WoS. Shares then fell almost 40% in January 2024 to settle at £3.7 as WoS issued a profit warning after Rolex reduced its UK allocation to WoS in December, a possible sign that Rolex was beginning to de-emphasize WoS and that a cyclical downturn was worsening. We believe instead that:

The chances of Rolex dis-intermediating WoS to any material extent in the next decade are minimal.

Rolex's decision to acquire Bucherer was motivated by Swiss heritage rather than profits.

Rolex's decision to reduce allocations in December was unrelated, not targeted at WoS, and that allocations for 2024 are 'back to normal'.

Above all, we believe that WoS's relationship with Rolex is likely to strengthen and its market share increase.

The day after the Bucherer announcement, WoS issued a press release with approval from Rolex (highlights added):

Rolex's press release the day before had similarly stated that "To preserve the long-standing partnership between the two companies and perpetuate their shared history, Rolex has decided to acquire Bucherer. The watch retailer will keep its name and continue to operate independently."

While this may appear to be marketing spin by Rolex in order to appease its retail base in the short term before bringing distribution inhouse in the long run, multiple former Rolex employees told us that was not the case. Instead, the Bucherer acquisition happened largely to preserve Swiss heritage and prevent a competitor like Swatch or LVMH from taking half of Rolex's retail network in Switzerland.

It is important to understand that Rolex does not think like a typical corporation. Rolex's founder - Hans Wilsdorf - set up the Hans Wilsdorf Foundation and the controlling interest of Rolex was transferred to it upon his death in 1960. Rolex is a non-profit where all cash is reinvested into the business or distributed, largely to the foundation.

Rolex does not attempt to maximize profits to maximize charitable donations either. Virtually all distributions of the foundation are limited to the district of Geneva and given the already incredible economics of Rolex the foundation actually faces the 'problem' of what to do with so much cash. Former employees and local people told us stories of the foundation saving historic theaters and sports teams from bankruptcy, buying real estate, and giving to public projects.

Rolex also reinvests cash internally and the 'problem' of having "too much money" as one former employee put itmeans that every building is the best of the best and equipped with elevators like luxury watches and five star restaurants. The working culture is low stress, with employees not being reprimanded for buying a €1mm machine that is never used, managers consciously retaining employees who work half as much as others, and working hours that are flexible.

Rather than focus on profits or the short term, former employees told us that Rolex's core goal is to ensure that the wonder and magic of its watches strengthens for generations to come. Every source we spoke to in Switzerland told us that profits were not the key goal, instead emphasizing words like heritage, prestige, and sustainability.

They also emphasized to us that Rolex CEO, Jean-Frédéric Dufour, is very unlikely to change the company's culture or goals, while the board and Wilsdorf family are even more conservative.

The Swiss newspaper Tribune de Geneve profiled the Wilsdorf Foundation in 2018, showing that most board members are from a social or public sector background.[2]

In fact, Rolex's charitable mindset extends not only to the foundation's giving. The company sees itself as a sort of guardian of the Swiss watch industry as a whole. And this may seem shocking to hedge fund managers, but Rolex deliberately leaves Swiss watchmaking talent and capacity to competitors so that the whole ecosystem can grow sustainably - it could easily damage or eliminate competitors but chooses not to.

A recent example of this sentiment was when Rolex came together with Patek Philippe and Richemont to form a foundation and host the now annual Watches and Wonders in Geneva, the industry leading trade show that is open to the public. The previous trade show had shut during Covid and sources told us this was an example of Rolex - which already sells every watch it makes - protecting the industry and smaller brands from external shocks.

Our sources told us that Rolex acquired Bucherer largely for the reasons it has stated publicly, with the primary reason being that Jorg Bucherer (who passed away shortly after) had no descendants and Rolex wanted to ensure that one of its most historic and Swiss retailers did not end up being owned by a private equity firm or a competitor.

They were also clear that Rolex does not intend on being a retailer itself, although our sources were split on whether WoS would see any impact from it owning Bucherer - some thought that on the margin Bucherer could be preferred for certain locations, while others expected no impact on WoS or even competitor watch brands. Either way, we do not expect this to be material as WoS is dominant in the UK where Bucherer has just 5% market share and is only in London, while there is a large amount of white space for both to expand in the US. The concern that WoS could be disintermediated appears very misplaced.

As Jake Ehrlich, founder of RolexMagazine.com and one of the world's leading Rolex historians and commentators, told us:

Investing in Watches of Switzerland is probably as close as someone can come to investing in Rolex. I would argue it's got to be one of the safest investments anybody could make as long as they don't get divorced. I think it's a 90% chance they would not get divorced. It would take Rolex getting really hot again and really aggressive, like changing the name of Bucherers to Rolex boutiques. I don't think they will. The only way it would happen is if Watches of Switzerland did something to turn Rolex off. They are as top tier as top tier gets. My understanding is next to Bucherer they are at the top. It would take a lot and my guess is they are highly aware…What's going to happen over the next couple decades? Consolidation. And Watches of Switzerland would likely be a beneficiary.

We are also not concerned that Rolex reduced its allocation to WoS in December 2023, shortly after the Bucherer acquisition. Data from the Federation of the Swiss Watch Industry shows that the value of all Swiss watch exports to the UK declined 41% month over month in December, meaning this was not isolated to WoS. The data also shows that exports have since rebounded, which is supported by WoS's stronger results so far in 2024.

Another investor concern has been that the luxury Swiss brand Audemars Piguet recently took distribution inhouse in order to control who becomes a customer. However, AP makes just 45,000 watches per year whereas Rolex makes over 1mm and plans to increase production by 60% over the next decade. It's also worth noting that AP has not eliminated retailers entirely as was initially feared and in fact is opening a 6,500 sqft flagship AP Town House with WoS in Spring 2025.

Our sources told us that brands tend to swing back and forth between bringing retail inhouse to gain control or outsource to improve distribution. Several brands that have opened their own stores have struggled to make a profit, and some are returning to outsourcing as a result.

Tellingly, WoS's senior management were in Geneva to meet Rolex shortly after the Bucherer acquisition announcement, and just a few weeks later publicly announced a new long range plan to FY28. The plan included a goal to more than double revenues and profits over five years and it is inconceivable that these targets would have been made without guidance and permission from Rolex.

We think it is very likely that WoS's relationship with Rolex continues to strengthen as it builds out increasingly marquee stores and helps elevate the customer experience in the US market like it has done in the UK, all at no cost to Rolex. But, in the unlikely scenario that Rolex did want to become a major retailer in the UK our sources saw only one option for Rolex - acquire WoS.

Concerns Over the Current Market Downturn are Overdone

We believe the second reason WoS stock has sold down is that the luxury watch market has been in a cyclical downturn since Q1 2022. Investors have been scared off by headlines such as this:

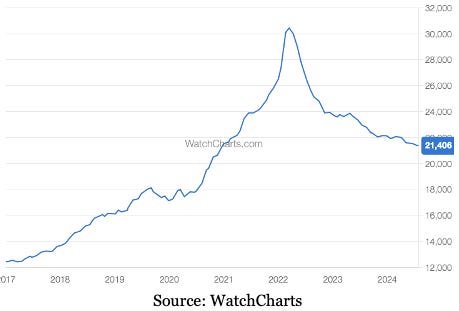

This type of analysis typically uses data from WatchCharts, which shows that an index of Rolex watches has declined in value by 30% since peaking in March 2022:

This represents the prices of Rolex watches on the secondary market, where people are reselling watches they have already bought from retailers like WoS in the primary market. A decline in secondary prices does not directly impact WoS. It is the primary market prices set by Rolex that matters for WoS, and Rolex does not cut prices. For context, Rolex has raised retail prices by roughly 5% per annum over the last 50 years, with larger increases during the 1970s when inflation was high and little or no increases during downturns like 2008-10.

Rolex is able to raise prices over time because it maintains the scarcity and desirability of its product through brand marketing and managed supply. While Rolex is not as aggressive in fostering undersupply and customer waitlists as Hermes, it is nevertheless careful not to flood the market with excess supply. These conditions mean a new Rolex is typically an appreciating asset. Historically customers could buy entry level watches on the same day or soon after visiting a retailer, but would only be able to buy higher end watches after making those initial purchases and registering for a waitlist.

That wait with no guarantee you will eventually get the watch you want caused the secondary market to develop, to the frustration of Rolex. Typically, the most desirable Rolexes sell on the secondary market for a 20-30% premium to retail prices, although this varies widely by model.

Things changed in 2020 when Rolex cut production by 30% during Covid lockdowns. At the same time, demand increased as the growth in financial assets, stimulus money, and restricted consumer spending led to a boom in disposable incomes. Waiting lists rocketed, causing frustrated consumers to turn to the secondary market to get their watches immediately.

This caused a spike in secondary market premiums that then attracted a technical rather than fundamental player - speculators who have no interest in watches, but buy them to flip on the secondary market for a profit. This cycle became self-fulfilling, with more speculators leading to more demand and therefore even higher premiums. We estimate that at its peak in March 2020 roughly one-third of Rolexes were being bought by people with no interest in watches and that premiums had spiked to over 100%, with the top models reaching 200%. WoS benefited to some extent from more people walking into its stores and buying other brands, with EBIT margins expanding from 8.6% in FY20 to 11.6% in FY22.

That has now reversed. As stock markets peaked in Q1 of 2022 so too did the secondary market for watches. Price declines caused speculators to become net sellers instead of net buyers, effectively causing a temporary de-stocking process. WOS's revenue growth slowed to 2% in FY24 despite the store count increasing 16%. The company cut its fiscal year guidance in January 2024 based on weak December trading in the UK, causing the stock to decline nearly 40% in two days. Subsequent data from the Federation of the Swiss Watch Industry shows that the value of Swiss watch exports to the UK declined 41% month over month in December.

The spread of secondary prices over retail is today back down to around 30%, while WoS's EBIT margins declined to 7.8% in FY24 or 8.8% excluding impairments. The company has also guided to margins in FY25 that we estimate are 8.2% if its acquisition of jewelry distributor Roberto Coin USA is excluded. In other words, secondary spreads and WoS's margins are largely back to normal. Swiss watch exports to the UK have also stabilized, declining only 1% y/y from January to June and growing 1% in July. WoS released a trading update in June in which it stated that "The UK market is starting to show signs of stabilisation". Export data also shows the US market grew 6.5% in June and 11.3% in July.

The most severe way a decline in secondary prices could impact WoS is if Rolex decided to cut supply to maintain the scarcity and premiums of its watches. We do not believe that will happen.

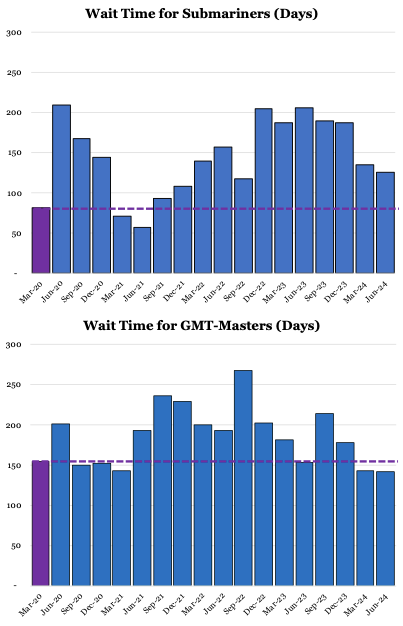

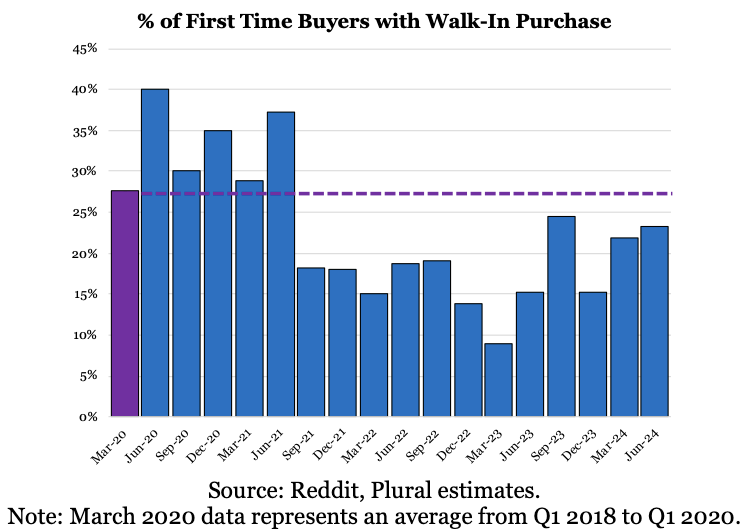

In our view, the best indicator of supply and demand is the current length of waitlists and how that compares versus history. We were able to estimate waiting times based on 3,262 messages on Reddit where customers described actual Rolex purchases. Each message included the date they received their watch, how long their actual wait time was, whether they had a prior Rolex purchase history, and the country the purchase was made from. Although messages on Reddit are likely to be made by particularly enthusiastic buyers who are more knowledgeable than the average customer and therefore the wait time for average customers is likely to be significantly longer, we believe the trends from this data are accurate.

What the data shows is that the wait times for Rolex's most prestigious brands, like Submariners and GMT-Masters, spiked in Q2 2020 as Covid lockdowns were initiated before returning to normal levels. However, as Rolex cut supply and speculators entered the market wait times increased again, peaking in late 2022. Wait times have since been declining, but crucially remain at or above pre-Covid levels.

Similarly, the percentage of new customers able to walk into a store and buy their first Rolex on the same day bottomed in late 2022 and has since returned to pre-Covid levels.

These data suggest to us the market has returned to normal rather than a downturn and there is no reason for Rolex to cut production and risk a repeat of the post-Covid bubble that resulted in speculators crowding out genuine customers.

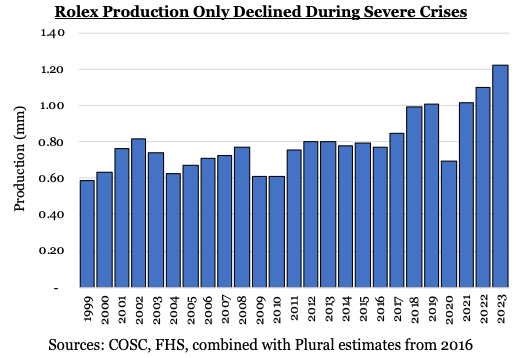

Indeed, we estimate that Rolex has historically cut production only in severe crises (e.g. post 9/11 & SARS, 2008 financial crisis), before recovering in 2-3 years. We do not believe the current environment is analogous, particularly in the US and UK where stock markets are near all time highs and interest rates are likely to decline. If Rolex were to reduce supply it would likely be to China, where real estate prices and the appetite for luxury spending continue to decline. A reallocation of supply from China to the US or UK would benefit WoS.

A Rolex also remains an appreciating asset. Retail prices have continued to increase and a buyer at the peak of the bubble in Q1 of 2022 would still be able to sell their watch on the secondary market today at a large premium to their retail purchase price. And more importantly, a long term customer who bought their watch a decade ago would have seen a very substantial appreciation.

In fact, we think that Rolex production is likely to increase. The company is currently building a new facility to increase production by 60% in 2029, with a temporary facility increasing production in 2025. That will likely drive a 60% increase in WoS's Rolex sales over the next five years, before market share gains.

After reading this report, read my latest analysis on WOSG’s upside, results, cycle, and growth runway, based on 59 interviews over two years and attendance at the industry’s leading trade show.

Governance

Watches of Switzerland was acquired by Apollo in 2013 and hired current CEO Brian Duffy and CFO Anders Romberg from Ralph Lauren in 2014. Although Apollo's initial strategy was to cut costs to increase FCF, Brian convinced them to instead invest to upgrade the customer experience in store that looked tired in order to grow the UK market. That strategy paid off, with WoS's UK market share of Rolex increasing from about 35% to 50% over the last decade and Rolex supporting the company to replicate its strategy in the US.

Apollo IPOed the company in 2019 and sold out entirely in 2020.

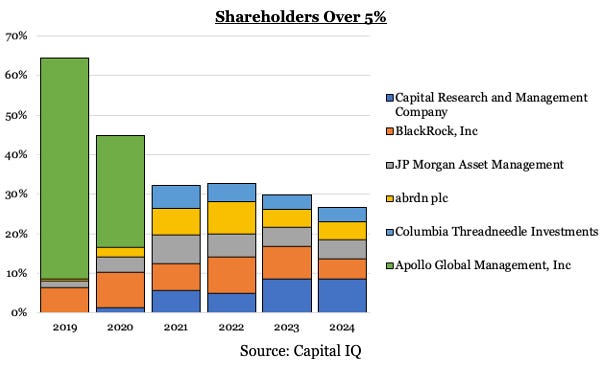

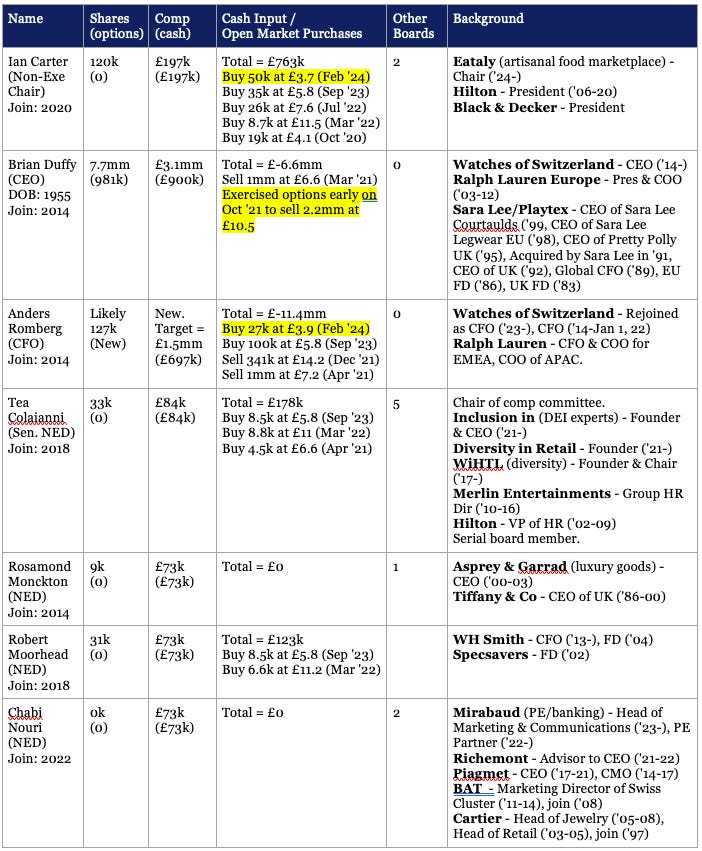

The company has no major active shareholders today, while stock ownership among non-executive board members is fairly low. However, Duffy is well incentivised with £32mm in shares and additional options and the Chairman and CFO bought shares at £3.7 in February after the stock fell heavily post results. The board also has good industry experience.

Overall, we believe the management at WoS are competent and experienced and that CEO Duffy is well incentivized.

Senior Management

The board has good industry experience and the CEO is well incentivized with £32mm in stock and additional options. However, stock ownership is low beyond the CEO and there are no investors on the board. Most board members have bought shares with their own cash, including the Chairman and CFO buying after the stock declined in February. The CEO's ownership has been entirely earned rather than acquired and he exercised options early in October 2021 to sell shares at £10.5, suggested he believed the stock was overvalued at the time. The CFO sold his shares prior to leaving for personal reasons in 2021 and has bought some shares since returning.

Related party transactions: None

AGM voting results: Each board member received 99% of votes in favor of their re-election at the 2023 AGM. 97% of votes were in favor of the compensation report.

Management Compensation

The CEO and CFO's comp are of a reasonable size and generally well structured, with the vast majority for the CEO contingent on adj EBIT, adj EPS, and adj ROCE. Adjustments are limited, although we would prefer the weighting on returns to be higher than the earnings numbers. The CEO has not received an increase in base salary since he joined in 2014.

Board compensation is reasonable.

Base:

£500k for the CEO, £380k for CFO.

The CEO's base is unchanged since he joined in 2014.

Bonus:

Target is 150% of base for the CEO, 125% for CFO.

100% on adj EBIT, subject to an ESG underpin which can reduce the bonus up to 10%.

2/3 paid in cash and 1/3 in deferred shares subject to a 3 year vesting period.

FY23 target = £153mm-£169mm. Achieved = £165mm. (Reported EBIT = £178mm, they adjusted down for IFRS changes. Post leases = £161mm, so limited adjustments upwards). Payout = 112.5% of base.

LTIP:

Target 200% of base for the CEO, 175% for CFO.

80% on adj EPS and 20% on ROCE. Both cumulative over 3 years.

FY24-26 targets: Cumulative EPS = 178.2p-196.9p, ROCE = 22.7%-25.1%. The mid-point implies average net income of £141mm per annum, while the high point (likely what management think is actually achievable) implies £150mm. Given growth over the three years this implies management think over £160mm is achievable in year 3, which would put the stock on a 6x P/E.

Subject to 24 month holding period.

Incentives for other senior management:

18 other members of management are eligible for an LTIP of 20-80% of base. From the FY23 annual report:

Our colleagues in support functions participate in the Company’s Annual Bonus Plan and are rewarded based on financial performance measured using Adjusted EBIT. As outlined on page 157 we have enhanced the ESG underpin that will apply to the annual bonus for FY24.

Bonuses typically operate in one of three formats depending on the level of seniority and line-of-sight to performance:

o For roles with a global remit, bonuses are based 100% on Group performance

o For roles that wholly or mainly concentrate on either our UK and Europe or the US operations, bonuses are based 100% on the performance of the business in the relevant country

o For certain business unit roles or regional roles, 50% of bonus is based on local performance (e.g. UK/US) and 50% is based on the performance of the relevant business unit

Management Quality

We spoke with multiple sources that have interacted with Duffy closely and came away with a positive impression.

Duffy has been hugely successful in having a very clear vision to upgrade and consolidate the UK and been able to build a company that then executed on that. He is unusual in being relentlessly focused on the financials as a Chartered Accountant but also charismatic and having marketing background.

Sometimes his natural optimism can spill in to investor communications, but Duffy believes what he says.

Part of his success has also been in managing the watch brands and particularly Rolex. Duffy has an excellent relationship with Rolex, which along with the company's execution in the UK convinced Rolex to allow WoS to try and replicate it in the US.

Although he owns a substantial amount of stock, we believe Duffy does not need the money. He was highly successful at Ralph Lauren and retired before being recruited by Apollo. He is passionate about the luxury watch market and working with his team, which includes several people who worked with him at Ralph Lauren.

One of those people is Anders Romberg, the CFO.

Romberg, a Swede with dry humour and a direct way of communicating, has worked with Duffy for nearly two decades. Romberg was working for Ralph Lauren in Hong Kong when Duffy convinced him to move to the less exotic location of Leicester in the UK to work with him.

The two have complemented each other well ever since, with Romberg knowledgeable about the operations beyond the financials and naturally more conservative than Duffy. Their shared experience allows them to have frank conversations with each other.

Romberg retired at the end of 2021 for personal reasons, and Duffy recruited him to return in 2023.

Duffy and Romberg are a highly competent and experienced duo who are doing the job because they are passionate about it.

Vision and strategy:

Management's vision is to extent its lead in the UK and become the leading retailer in the US by replicating the strategy that has worked so well in the UK. By investing to upgrades stores in the UK, WoS was able to attract more customers and ultimately higher Rolex allocations as Rolex increased production and pulled allocations from mom & pops.

This strategy will involve using all cash generated for store renovations, acquisitions, and M&A. The company's Long Range Plan includes the goal to double revenue and EBIT from FY23 to FY28 and targets UK growth of 8-10% and US growth of 20-25%. Jewelry as a portion of revenue is likely to increase modestly, with the company spending $130mm to acquire Robert Coin's US distribution in May 2024.

Management's use of cash reflects this focus on capex and M&A. From FY20-24 the company's cash generation and use was (adjusted to US GAAP instead of IFRS):

Operating cash flow (ex. SBC, WC) = £569mm

Working capital = £-83mm

Net capex vs D&A = £-245mm vs £140mm D&A

M&A = £-144mm (acquired Roberto Coin for $130mm post FY24)

Dividends = £0mm

Debt = £-185mm

Equity (inc. SBC) = £136mm (£155mm issued at IPO).

Others = £-33mm

= Net change in cash = £81mm

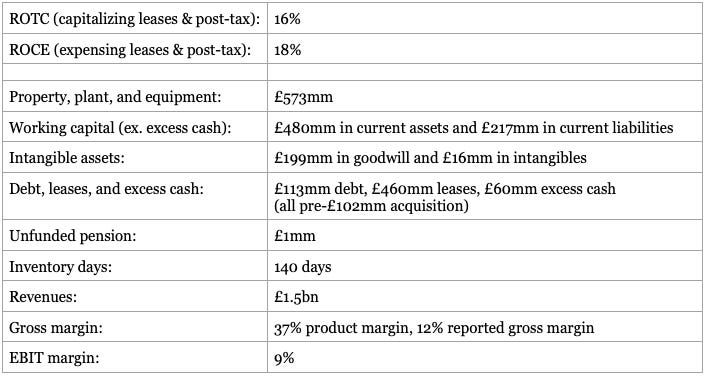

Over the five years invested capital (ex leases) has increased from £244mm to £520mm, with no dividends paid. Sustaining FCF, calculated as EBIT after lease expenses and tax but excluding exceptionals, increased from £43mm to £93mm. That implies management deployed capital at incremental returns of 20%, slightly above the group average.

Investments in systems such as CRM software have also made the company more efficient, with sales per employee increasing by over 40% from £408k in FY19 to £582k in FY24, and inventory days reducing by 20% from 174 days to 140 days.

Track record of success:

Duffy and Romberg have executed well over the last decade. We estimate WoS's share of Rolex sales increased from 35% to 47% in the UK from 2015 to 2024. While revenues and EBIT increased by 18% p.a. and 32% p.a. over this period. Post-tax returns on tangible capital increased from 8% to 17%. Management's success encouraged Rolex to let them implement a similar strategy in the US.

The stock's performance has not reflected management's execution in our view. The company IPOed at £2.7/shr in 2019 and rose to £15 by 2022 before declining to £4.1 today for a return of 9% p.a. That is still a significant outperformance of the UK's FTSE Aim All-Share index, which has returned -3% p.a. over this period, while the Russell 2000 has returned 8% p.a.

Customer focus:

Management has a strong focus on customer service, with Duffy's strategy largely focused on investing to improve the customer experience. That resulted in more luxurious but less intimidating stores, and customers being offered drinks and snacks when entering a Rolex shop, etc. Our anecdotal evidence and data from Google reviews and other websites suggests WoS's customer service is best in class.

There is a subset of customers who have had a poor experience because they were not able to purchase a Rolex or the Rolex they wanted, but to a large extent that is a feature rather than a bug of the Rolex experience and largely out of WoS's control.

We also believe that to a great extent WoS's customer is actually Rolex, rather than the person walking into its store.Every Rolex watch largely sells itself and has a fixed margin and it is Rolex that determines how many watches WoS gets and where it can open stores. WoS has done such a good job delighting its customer (Rolex) that it has been allocated an increasing share of the UK and US markets. We believe that as long as WoS continues to execute it is closer to a subsidiary of Rolex than a retailer.

Integrity:

Management score highly on integrity. A few examples include voluntarily returning government Covid furlough money, making limited adjustments to earnings for compensation targets, and Duffy maintaining the same base salary since 2014 when he could be extracting more from shareholders.

Duffy's natural optimism can occasionally spill in to investor communications, but we think he believes what he says.

Valuation

Is this a one foot hurdle or three foot hurdle?

One foot

Is this a cyclical or secular grower?

Currently going through a cyclical downturn, but we believe the big story is the secular growth in the US.

How could this be a value trap?

If post-Covid margins are an aberration.

Is this a cigar butt? Is this an appreciating/depreciating asset? Productive/Non-productive?

This is not a cigar but and is a productive and appreciating asset.

Is there an agency cost?

No.

Should valuation assume good or bad management execution?

Good execution. Management has a strong record.

Is this a turnaround story? (Base rates for success are low)

No.

Is this a company with big promises/hopes but little track record?

No.

Is this a single product company and/or is there a fad risk?

Rolex is by far the most valuable brand the company works with, but we are confident in the relationship.

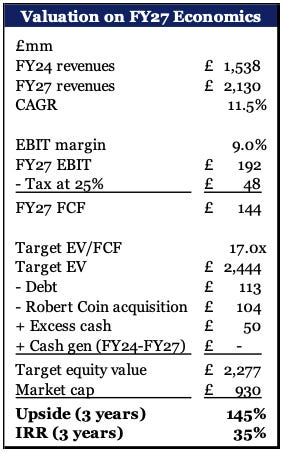

Base Case Valuation

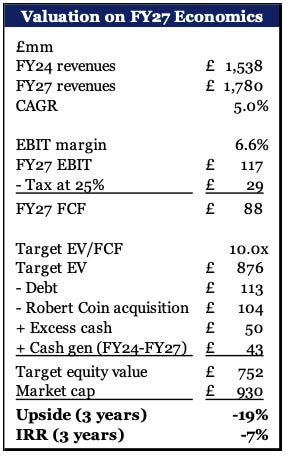

We believe that Watches of Switzerland shares can generate a 35% IRR over the next three years, for a 145% total return.

Our valuation assumes revenue and EBIT growth misses management's target of 15% p.a. over five years, as well as LTIP targets that imply average net income of £141mm p.a. from FY23-25. We also assumed that EBIT margins stay flat at 9%, with support from operating leverage offsetting some additional compression in the luxury watch market. We assumed all FCF generated over the next three years is used to acquire business at 10x FCF. For context WoS acquired Roberto Coin in May at 6x FCF, although we think that was an unusually attractive deal.

We reached our target EV/FCF multiple of 17x using both comparable and historic multiples.

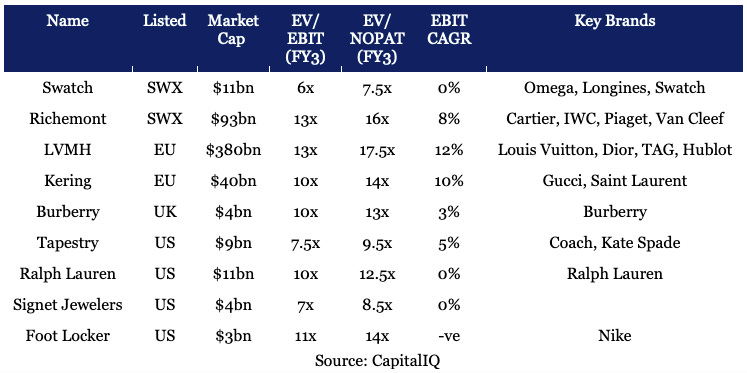

Luxury companies like LVMH and Richemont trade at 16-18x FY3 NOPAT with about 10% growth. Premium companies like Ralph Lauren, Burberry, and Tapestry trade at 10-13x with low single digits growth. Signet Jewelers, a jewelry retailer, trades at 8.5x with no growth. Foot Locker, which receives priority from Nike, trades at 14x.

We do not believe WoS deserves the multiple of luxury brand owners like LVMW and Richemont. However, given WoS has 10%-15% growth we believe a 13x FY3 multiple is reasonable, similar to premium brands that have less growth. That implies 17x trailing earnings.

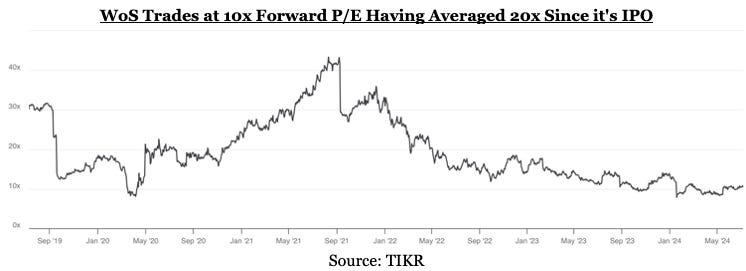

WoS has historically traded at an average 20x forward P/E since its IPO in 2019, with the multiple declining to 10x today based on concerns over Rolex and a cyclical decline. We think 17x trailing FCF is in keeping with a partial return to historic multiples as investor concerns around these issues reduce.

WoS Trades at 10x Forward P/E Having Averaged 20x Since it's IPO

Bear Case Valuation

We think it is hard to lose large amounts of money over a three year horizon by investing in WoS, and have 20% downside using a scenario where Rolex neither increases nor decreases supply and other brands cut production by 20%. To be clear, our valuation is based on fundamentals and sentiment could drive the stock below that over shorter periods of time.

While Rolex is increasing production by 60% by 2029 and our data suggests waitlists remain at normal levels and provide a buffer, this scenario assumes that conditions worsen to such an extent that the increase in production is scrapped.

We further assume that the non-waitlist brands cut a combination of supply and price by 15%. For context, the value of Swiss watch exports declined by 28% in 2009 but fully recovered two years later. Our Bear case assumes a 15% decline with no recovery despite US and UK stock markets near all time highs, interest rates likely to decline, and watch export growth of 6.5% and 11.3% in the US and -2.3% and 1.0% in the UK between June and July.

We assume a revenue growth of just 5%, which given the acquisition of Roberto Coin and the existing pipeline of store openings implies around 5% declines p.a. in same-store-sales. For example, the acquisition of Roberto Coin also adds £105mm in revenues, while we believe the upcoming 8,000 sqft Rolex store on Bond St could generate £65mm in revenues and the 6,500 sqft AP Town House could generate around £40mm.

We model EBIT margins declining from management's guidance of 9.1% for FY25 to 6.6%, in line with what our unit economics suggest the drop through is from a decline in non-waitlist brand sales, plus a decline assuming that Roberto Coin sold partially because it was overearning.

We assume a knock-on effect of the slowdown is that inventory days expand by about 30% to levels last seen in 2016, sucking in cash generated. In this scenario the company makes no material acquisitions with the remaining cash it generates.

Finally, we assume investors value the stock at 10x FCF, in line with valuations for lower quality peers who have limited growth. This valuation is below Foot Locker, which has seen EBIT margins cut from 7.4% to 2.3% in FY 24 and trades at 19x consensus FY25 NOPAT and 14x FY26. Foot Locker has a similar but weaker relationship with Nike, which gives Foot Locker priority access to the best sneakers. Nike has no wait list like Rolex, faces discounting, theft, has opened its own stores, is selling online, and faces competitive threats from new brands. In other words, virtually all the major risks that investors see with WoS/Rolex have actually materialized with Foot Locker/Nike, and yet Foot Locker still trades at a premium valuation to WoS.

Variant View & Catalyst

Why does this opportunity exist?

The stock is oversold because of concerns around Rolex acquiring a retailer, and the current cyclical downturn in the UK luxury watch market.

Market Cap: £930mm

Volume: £5mm/day

Number of days float turns over (excludes 5%+ holders): 178 days

Sell-side coverage: 11

Buy-side coverage (Last 5 years):

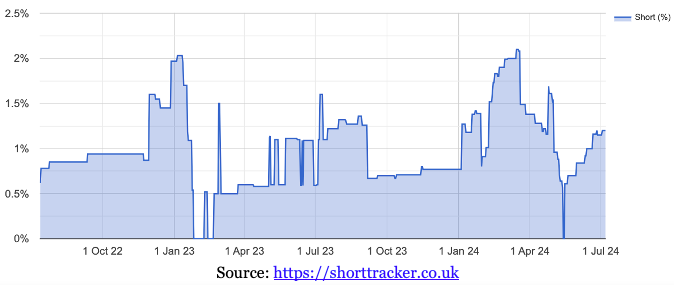

Short interest: ~2%

% of float owned by retail investors: 10%

Variant view

Our variant view is that WoS's relationship with Rolex is as strong as ever, the company has a structural growth opportunity with Rolex in the US that is underappreciated, and that the cyclical downturn is plateauing and a relatively small driver of WoS's intrinsic value.

Catalyst

No hard catalyst, but we think the market will be surprised by the contribution of WoS's new flagship stores such as on Bond St in London. We that WoS will succeed in doubling revenues and EBIT in its five year plan, which investors are skeptical of.

Short Interest

Share Price

After reading this report, read my latest analysis on WOSG’s upside, results, cycle, and growth runway, based on 59 interviews over two years and attendance at the industry’s leading trade show.

If you found this report useful, subscribe to receive:

Special Reports: 30 pages beginning with a 1 page summary on a long-term investment idea, based on discussions with 20 industry experts. Expect 3 reports per year and extensive follow-up work.

Deep Dives: 5 page writeups on long-term investment ideas based on extensive primary research. Expect 2 per year.

Notes from the Trade Show: In-depth analysis from attendance at industry events relevant to the stocks we have written about.

Monthly Updates: New updates at 11am EST on the first Tuesday of every month with work on the stocks we profiled, including relevant industry news and results.

Important Disclosures

This newsletter is not investment advice. The goal is to provide value-added work, but you should always do your own research and make your own decisions. Any assertons made in Hidden Gems Investing represents the author’s opinion and do not necessarily represent the views of Plural Investing.

THE INFORMATION CONTAINED ON THIS WEBSITE IS NOT AND SHOULD NOT BE CONSTRUED AS INVESTMENT ADVICE, AND DOES NOT PURPORT TO BE AND DOES NOT EXPRESS ANY OPINION AS TO THE PRICE AT WHICH THE SECURITIES OF ANY COMPANY MAY TRADE AT ANY TIME. THE INFORMATION AND OPINIONS PROVIDED HEREIN SHOULD NOT BE TAKEN AS SPECIFIC ADVICE ON THE MERITS OF ANY INVESTMENT DECISION. INVESTORS SHOULD MAKE THEIR OWN DECISIONS REGARDING THE PROSPECTS OF ANY COMPANY DISCUSSED HEREIN BASED ON SUCH INVESTORS’ OWN REVIEW OF PUBLICLY AVAILABLE INFORMATION AND SHOULD NOT RELY ON THE INFORMATION CONTAINED HEREIN.

The information contained on this website has been prepared based on publicly available information and proprietary research. The author does not guarantee the accuracy or completeness of the information provided in this document. All statements and expressions herein are the sole opinion of the author and are subject to change without notice.

Any projections, market outlooks or estimates herein are forward looking statements and are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur. Other events that were not taken into account may occur and may significantly affect the returns or performance of the securities discussed herein. Except where otherwise indicated, the information provided herein is based on matters as they exist as of the date of preparation and not as of any future date, and the author undertakes no obligation to correct, update or revise the information in this document or to otherwise provide any additional materials.

The author, the author’s affiliates, and clients of the author’s affiliates may currently have long or short positions in the securities of certain of the companies mentioned herein, or may have such a position in the future (and therefore may profit from fluctuations in the trading price of the securities). to the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

Neither the author nor any of its affiliates accepts any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of the information contained herein. In addition, nothing presented herein shall constitute an offer to sell or the solicitation of any offer to buy any security.

[1] Source: Companies House. Bucherer UK: £102mm in revenues and £1.2mm in capex, Laing The Jeweller (Glasgow) Ltd: £63mm in revenues and £2.8mm in capex, David M Robinson: £55mm in revenues and £4.0mm in capex.

[2] https://www.tdg.ch/wilsdorf-plus-quun-mecene-une-vraie-machine-a-cash-797828901292